By Jeff Lambert | The Lambert Agency | Austin, TX | Estimated Read: 20–25 Minutes

If you’ve ever sat across from an insurance broker and heard the phrase “Indexed Universal Life insurance,” chances are your eyes glazed over somewhere around the word “indexed.” You are not alone. IUL policies are one of the most powerful — and most misunderstood — financial tools available to everyday Americans today, and the confusion is entirely understandable. At The Lambert Agency in Austin, Texas, we work with families, business owners, and high-income professionals every single day who come to us frustrated, under-protected, and unsure whether their current financial strategy is actually doing what they think it is.

Many of them, after an honest conversation, discover that an Indexed Universal Life insurance policy was the answer they did not know they were looking for.

This guide exists to change that narrative. Whether you are a first-time insurance buyer trying to understand what an IUL even is, a business owner wondering how to protect your income and your business simultaneously, or a seasoned saver questioning whether your 401(k) alone is going to carry you through retirement — this article will walk you through every critical angle of IUL policies in plain, honest language.

We are going to cover the core benefits of IUL policies, answer the most common questions people ask us here at The Lambert Agency, and help you understand whether an Indexed Universal Life insurance policy deserves a place in your long-term financial plan. We will also explore how IUL fits into the broader financial landscape — comparing it to whole life, term life, Roth IRAs, and 401(k) plans — so you can make a fully informed decision. Let us get into it.

1. What Is an IUL Policy and How Does It Work?

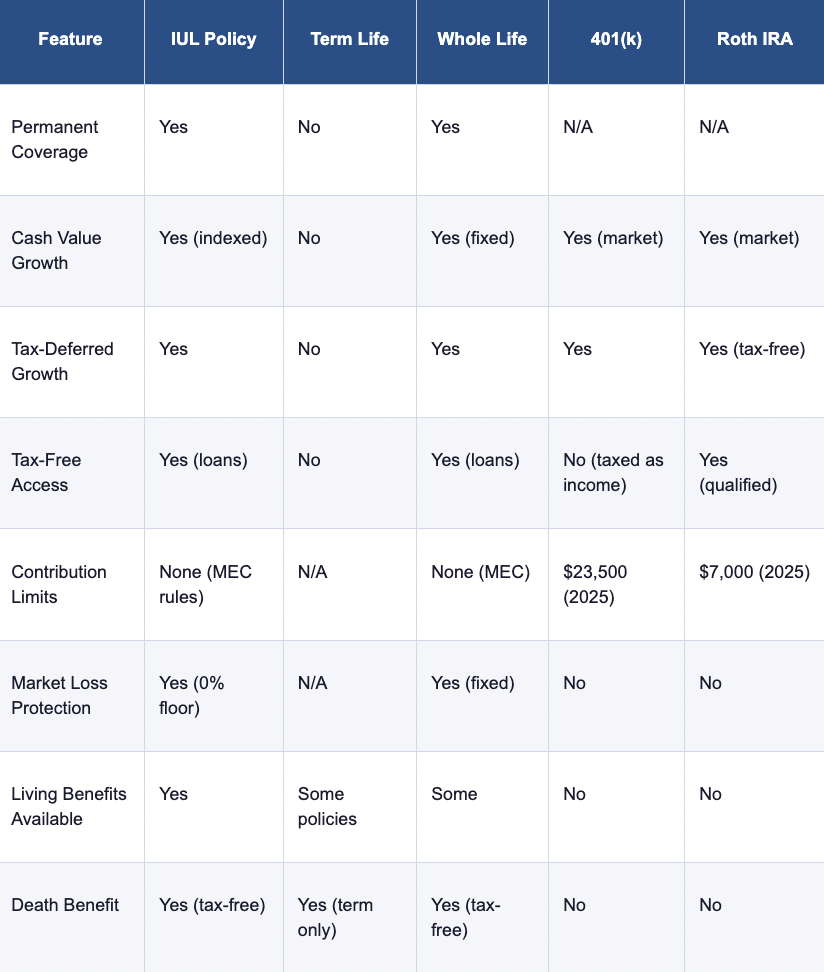

Before we talk about benefits, you need a solid understanding of the product itself. An Indexed Universal Life insurance policy — most commonly called an IUL — is a form of permanent life insurance that combines a tax-free death benefit with a growing cash value account. Unlike a traditional whole life insurance policy, which credits interest at a fixed rate determined by the carrier, an IUL ties the growth of your cash value to the performance of a major stock market index, most commonly the S&P 500.

Here is the most important distinction that separates an IUL from actually investing in the stock market: your money is never directly invested in equities. Instead, the insurance carrier uses a portion of your premium to purchase financial instruments — typically options contracts — that mirror the movement of a chosen index. This structure allows you to participate in market gains during strong years, while a contractual guarantee protects your cash value from going backward when markets decline.

How does an IUL protect my money during a market downturn?

This protection is made possible through two core mechanisms built into every IUL policy:

• The Floor: Most IUL policies guarantee a minimum crediting rate of 0%. This means if the S&P 500 drops 35% in a single year — as it did in 2008 and again briefly in early 2020 — your cash value does not decrease due to index performance. You keep every dollar you have accumulated. You do not lose a cent to the market.

• The Cap: In exchange for that downside protection, the insurance carrier places a ceiling on the maximum gain you can receive in any given crediting period. If your cap is 12% and the S&P 500 gains 22%, you receive 12%. Your upside is capped, but your principal is preserved and your gains lock in permanently each year.

Some IUL products also incorporate a participation rate — the percentage of the index’s gain you are credited before the cap is applied. A participation rate of 80% on a year when the index gains 15% would credit you with 12% (80% of 15%) before the cap. Understanding all three variables — floor, cap, and participation rate — is essential to evaluating the true performance potential of any IUL policy. This is exactly the kind of side-by-side analysis we perform with every client at The Lambert Agency.

2. What Are the Main Benefits of an IUL Policy?

This is the question that brings most people to our office or to this article. The benefits of an Indexed Universal Life insurance policy are significant, and they span financial planning, tax strategy, retirement income, legacy building, and business continuity. Let us break each one down in full.

How does an IUL provide a tax-free death benefit for my family?

The most foundational benefit of any life insurance policy is the death benefit — the lump-sum payment made to your beneficiaries when you pass away. Under current IRS tax law, life insurance death benefits are received income-tax-free by your heirs. For families in Austin and across Texas who are thinking about leaving something meaningful behind, this is often the starting point of the conversation.

What makes the IUL’s death benefit uniquely valuable compared to term life insurance is that it is permanent. Term life insurance expires. If you purchase a 30-year term policy at age 32 and are still alive at 62, your coverage ends and you walk away with nothing. An IUL, properly structured and consistently funded, can provide a meaningful death benefit for your entire life — regardless of when that day comes.

For business owners, the death benefit also plays a critical role in buy-sell agreements, key person insurance strategies, and executive compensation plans, all of which we explore in a dedicated section below.

How does an IUL build tax-deferred cash value?

Every premium payment you make into an IUL policy above the cost of insurance goes into your cash value account. That account grows on a tax-deferred basis — meaning you do not owe income taxes on the interest credited each year as it accumulates. This is the same tax advantage that makes IRAs and 401(k) plans so attractive for retirement savings, but as we will explain shortly, the IUL carries that advantage significantly further.

Tax-deferred compounding is one of the most powerful forces in personal finance. Because you are not losing a portion of your annual gains to the IRS each year, more money stays inside the policy and compounds on itself. Over a 20 or 30-year accumulation horizon, the difference between tax-deferred and taxable growth can represent hundreds of thousands of dollars in final account value.

Can I access money from an IUL without paying income taxes?

Yes — and this is where Indexed Universal Life insurance separates itself from nearly every other financial vehicle available to the American consumer. Under current IRS tax code, specifically Internal Revenue Code Section 7702, loans taken against the cash value of a properly structured life insurance policy are not considered taxable income. You are borrowing against your own policy, not making a withdrawal from a taxable account.

This creates a mechanism for generating tax-free income during retirement that is genuinely distinct from what a 401(k) or traditional IRA can offer. Every dollar you pull from a traditional 401(k) in retirement is taxed as ordinary income — at whatever rate Congress decides that income tax bracket should be in the year you take the distribution. With an IUL structured correctly, you can take policy loans and certain withdrawals that are entirely free from income tax under current law.

For high-income professionals and business owners in Austin who are already maxing out their 401(k) and Roth IRA contribution limits, an IUL offers an additional tax-advantaged bucket with no IRS contribution cap. This is a major advantage that is frequently overlooked in conventional financial planning conversations.

3. IUL vs. Other Financial Products: How Does It Compare?

One of the most important conversations we have with clients at The Lambert Agency is the context conversation — where does an IUL fit relative to everything else? Here is a clear, honest breakdown.

Is an IUL better than a Roth IRA for retirement income?

This question comes up constantly, and the honest answer is: they serve different purposes, and the best clients often use both. A Roth IRA is an excellent vehicle with a critical limitation — the annual contribution cap. In 2025, you can contribute only $7,000 per year to a Roth IRA ($8,000 if you’re over 50), and higher-income earners may be phased out of eligibility entirely. An IUL has no contribution cap set by the IRS — the only constraint is the Modified Endowment Contract (MEC) rules, which prevent you from overfunding the policy in the first seven years in a way that would disqualify it as life insurance. Within those rules, a properly designed IUL can absorb significantly more capital than any Roth IRA.

Additionally, Roth IRA assets are subject to full market risk. A severe market downturn the year before or the year you retire can devastate a Roth IRA balance. An IUL’s 0% floor ensures that kind of scenario does not erase years of compounding. For clients approaching retirement, sequence-of-returns risk is a very real threat — and the IUL structure provides a genuine hedge against it.

How does an IUL compare to whole life insurance?

Both IUL and whole life insurance are permanent policies with tax-advantaged cash value. The core difference is in how that cash value grows. Whole life uses a fixed, guaranteed interest rate set by the insurer — typically between 2% and 4% historically. This offers extreme predictability. An IUL’s potential return is higher in most market environments — historically averaging between 5% and 8% depending on index performance, caps, and participation rates — but is less guaranteed because it is tied to an index.

Whole life is often the right choice for clients who prioritize absolute certainty and guaranteed growth. IUL tends to be preferable for clients who want the potential for higher long-term accumulation while still maintaining downside protection. At The Lambert Agency, we help you evaluate which structure aligns with your specific risk tolerance, financial timeline, and goals.

Is an IUL a good alternative to a 401(k) for high-income earners?

An IUL is not a replacement for a 401(k) — especially when your employer offers matching contributions, which represent an immediate 50% to 100% return on those dollars. Always capture your full employer match first. However, once you have done that, and once you have maxed your 401(k) and Roth IRA contributions for the year, an IUL becomes a highly compelling next vehicle for tax-advantaged accumulation. The combination of unlimited contributions, tax-deferred growth, and tax-free access through policy loans creates a retirement income strategy that complements — and in many ways improves upon — the traditional 401(k) structure, particularly for those who expect to be in a higher tax bracket in retirement than they are today.

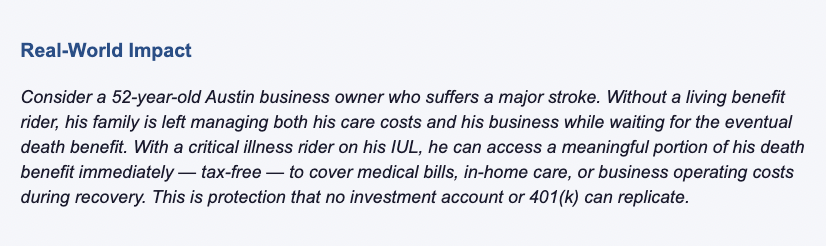

4. What Are Living Benefits on an IUL Policy, and Why Do They Matter?

One of the most underappreciated features of modern IUL policies is the availability of living benefits — also called accelerated death benefit riders. These provisions allow you to access a portion of your death benefit while you are still alive if you experience a qualifying health event. Depending on the carrier and policy, these events may include:

• Terminal illness diagnosis (typically life expectancy of 12 to 24 months or less)

• Chronic illness that impairs your ability to perform two or more activities of daily living

• Critical illness such as a heart attack, stroke, invasive cancer, or organ failure

• Critical injury resulting in severe and permanent cognitive or physical impairment

In a state like Texas, where healthcare costs can be staggering and where no state income tax means we often see higher-earners accumulating more in liquid assets, a living benefit rider can be the difference between financial security and financial ruin during a major health crisis. Many of these riders come at no additional premium cost — they are built into the base policy by the carrier.

At The Lambert Agency, we make it a point to ensure every IUL policy we design includes a thorough evaluation of available living benefit riders. These provisions are not add-ons — they are a core component of comprehensive life insurance planning.

5. How Can an IUL Policy Create Tax-Free Retirement Income?

This is perhaps the single most compelling reason that high-income professionals, business owners, and financially savvy individuals are turning to IUL policies as a cornerstone of their retirement strategy. Let us walk through exactly how it works.

How do policy loans generate tax-free income in retirement?

After years of consistent premium payments, the cash value inside your IUL policy has grown substantially — shielded from market losses and compounding on a tax-deferred basis. When you reach your retirement income years, instead of withdrawing money from a taxable account, you take loans against your policy’s cash value. The insurance carrier uses your cash value as collateral for these loans, and the outstanding loan balance continues to earn index-linked interest on your behalf.

Because policy loans are not considered income by the IRS under current tax law, you receive this money without triggering a tax event. Done properly — with guidance from an experienced broker who understands policy loan mechanics — this strategy can produce a meaningful and completely tax-free income stream throughout your retirement years.

The policy loan balance, plus accrued interest, is typically repaid from the death benefit when you pass away. This means your heirs still receive a death benefit — reduced by the outstanding loan — tax-free. Properly managed, this is one of the most elegant and efficient income strategies in all of personal finance.

What is the ideal age to start an IUL policy for retirement planning?

The best time to start is always earlier than you think. The power of an IUL in retirement planning is directly tied to the length of your accumulation period. A policy started at age 30 with consistent, properly sized premiums over 30 years will dramatically outperform a policy started at age 50 with the same annual premium, simply because of the compounding runway.

That said, we regularly help clients in their 40s and 50s design IUL strategies that are still highly effective, particularly when they have higher incomes that allow for larger premium payments and faster cash value accumulation. The key is to work with a broker who will design the policy correctly from day one — with a premium structure and death benefit sizing that maximizes cash value growth within IRS guidelines.

At The Lambert Agency, we have designed policies for clients at virtually every age and income level across Austin and Central Texas. Each one is custom-built, not pulled off a shelf.

6. How Can Business Owners in Texas Use an IUL Policy?

Indexed Universal Life insurance is not just a personal financial planning tool. For business owners across Austin, Central Texas, and beyond, IUL policies serve a range of critical business functions that most conventional planning conversations never address. Here are the most powerful applications:

Key Person Insurance

If your business relies heavily on one or two key individuals — founders, top salespeople, technical experts — the sudden death or disability of that person could threaten the company’s survival. A key person IUL policy, owned by the business, provides a tax-free death benefit that the company can use to recruit and train a replacement, cover revenue disruptions, or satisfy creditors and investors who may otherwise pull their support.

The cash value that accumulates inside a key person IUL policy is also a corporate asset — one that appears on the balance sheet and can be accessed for business operating needs during the owner’s lifetime.

Buy-Sell Agreement Funding

When a business has multiple owners, a buy-sell agreement defines what happens to each owner’s interest if one of them dies, becomes disabled, or decides to exit. IUL policies are a popular and highly effective vehicle for funding these agreements. Each owner can be insured under a policy that provides the liquidity needed for the surviving owners to purchase the departing owner’s interest — preventing the estate from forcing the company into a fire sale or bringing in an unwanted third party as a new partner.

Executive Bonus Plans and Deferred Compensation

Many privately held businesses in Austin use IUL policies as a platform for retaining top talent. Under an executive bonus plan — sometimes called a Section 162 bonus plan — the company pays the premium on an IUL policy owned by the key employee. The employee owns the policy personally, and the cash value belongs to them. The company receives a tax deduction for the bonus payment as a business expense. This structure provides a powerful retention incentive without the complexity and regulatory burden of a qualified retirement plan.

Similarly, nonqualified deferred compensation plans can be informally funded using IUL policies, allowing business owners to defer income for select executives in a tax-advantaged structure while building cash value that can support those future obligations.

7. What Are the Risks of an IUL Policy, and How Do You Avoid Them?

At The Lambert Agency, we believe in full transparency. We are not here to sell you a product — we are here to help you make the right decision. And the right decision requires an honest conversation about the risks and limitations of IUL policies as well as their benefits.

What is the downside of an IUL policy?

Every financial product involves trade-offs, and an IUL is no exception. Here are the most important limitations to understand before purchasing a policy:

• Complexity: IUL policies are more complex than term life or whole life insurance. The interplay of caps, floors, participation rates, policy charges, and loan mechanics requires careful design and ongoing management. A poorly structured IUL can underperform significantly or even lapse if premiums are not sustained.

• Caps limit upside: In a strongly performing market year — 2021, for example, when the S&P 500 gained approximately 27% — an IUL policyholder may only receive 10% to 14% depending on their cap rate. This is still a meaningful gain with zero risk of loss, but it is not the full market return.

• Internal Policy Costs: IUL policies carry internal charges for insurance costs, administrative fees, and rider costs. These are deducted from your premium before the cash value is credited. In the early years of a policy, these charges can meaningfully reduce the amount accumulating in your cash value account. This is why IUL is generally most effective as a long-term strategy — ideally ten or more years.

• MEC Risk: Overfunding a policy in the first seven years can trigger Modified Endowment Contract status, eliminating the tax-free loan advantage. This is why proper design from a knowledgeable broker is not optional — it is essential.

• Carrier Risk: While your cash value is not invested in the market, it is held by the insurance carrier. Choosing a highly rated, financially stable insurer is a critical step in the policy design process. At The Lambert Agency, we work exclusively with top-rated carriers and we review carrier financial strength ratings with every client.

8. Can an IUL Policy Help Fund a Child’s College Education?

This is a lesser-known but genuinely compelling application of an IUL policy. Parents across Texas are discovering that an IUL policy opened early in a child’s life can serve as a highly flexible college funding vehicle that complements or outperforms a traditional 529 plan in several key ways.

IUL vs. 529 Plan for College Savings: What Are the Key Differences?

• Flexibility: 529 plans must be used for qualified education expenses or face taxes and a 10% penalty on earnings. An IUL’s cash value can be used for anything — college tuition, a business startup, a home purchase, or retirement income — without penalty.

• Financial Aid Impact: Assets in a 529 plan are counted in federal financial aid calculations. Cash value inside a life insurance policy is generally not counted as an asset on the FAFSA, potentially preserving eligibility for need-based aid.

• Market Risk: A 529 plan invested in age-based funds can lose significant value right before your child needs the money, as happened to many families in 2008 and 2022. An IUL’s 0% floor means the balance you have built cannot be erased by a market downturn.

• Death Benefit: A 529 plan provides no life insurance protection. An IUL on the parent or the child provides a tax-free death benefit as an additional layer of security for the family.

A policy opened on a child at age 1 or 2, with consistent modest premiums over 17 years, can produce a meaningful cash value account by college age — all tax-deferred, accessible tax-free via loans, and carrying a growing death benefit throughout. Many of our Austin-area clients use this strategy as part of a broader family financial plan.

9. How Do You Choose the Best IUL Policy? What Should You Look For?

Not all IUL policies are created equal. The insurance marketplace is filled with products that vary dramatically in their fees, cap rates, participation rates, carrier financial strength, rider availability, and overall design philosophy. Choosing the wrong policy — or working with a broker who is captive to a single carrier and can only offer one product — can mean settling for a policy that significantly underperforms what the market can offer you.

What makes The Lambert Agency different when it comes to IUL design?

The Lambert Agency is an independent insurance agency. We are not tied to any single insurance carrier, which means we are free to compare IUL products from multiple top-rated insurers to find the policy that genuinely best fits your financial goals, your timeline, your risk tolerance, and your budget. We do not get paid more to recommend one carrier over another — our only incentive is finding the right solution for you.

Here are the key criteria we evaluate when designing an IUL policy for every client:

• Carrier Financial Strength: We exclusively recommend carriers with strong ratings from AM Best, Moody’s, and Standard and Poor’s. The insurer’s ability to honor its long-term commitments to you is foundational.

• Historical Cap and Participation Rate Performance: We analyze how the carrier has managed its cap and participation rates over time — not just what they are today. Carriers that have consistently lowered caps after the policy is issued are a red flag.

• Internal Fees and Cost of Insurance Structure: High internal fees erode cash value accumulation. We model the actual net performance of each policy after all fees to ensure we are comparing apples to apples.

• Illustration Assumptions: We review policy illustrations carefully to ensure they use realistic, conservative assumptions rather than the maximum allowable crediting rates that some agents use to inflate projected numbers.

• Available Riders: We confirm that the policy includes the living benefit riders, waiver of premium provisions, and other protective features that are most relevant to your situation.

• Policy Design Optimization: We design each policy to maximize cash value accumulation within IRS guidelines — using strategies like minimum death benefit sizing and appropriate premium structuring to ensure your dollars are going to work as hard as possible.

10. How Do I Get Started with an IUL Policy in Texas?

Getting started with an IUL policy does not have to be complicated. At The Lambert Agency, we have made the process as simple and transparent as possible. Here is what working with us looks like from your first conversation to your policy in force:

Step 1: Schedule a No-Obligation Strategy Call

The first step is a conversation — not a sales pitch. We want to understand your financial goals, your current coverage situation, your income, your family structure, and your timeline. Only when we understand your full picture can we begin evaluating whether an IUL is the right tool and, if so, how it should be designed for your specific needs.

Step 2: Receive a Custom Policy Design and Illustration

Based on what we learn in your strategy call, we will design a custom IUL policy illustration — comparing products from multiple top-rated carriers — that projects your cash value growth, loan availability, and death benefit over your target time horizon. We will walk you through every number, explain every assumption, and answer every question until you feel completely confident in the analysis.

Step 3: Complete the Application and Underwriting

Once you decide to move forward, we guide you through the application and underwriting process. Most IUL policies require a health questionnaire and, depending on your age and coverage amount, a brief medical exam. We handle all the paperwork and coordinate directly with the carrier on your behalf.

Step 4: Policy Delivery and Ongoing Service

Once your policy is approved and issued, we deliver it to you and walk you through every provision. This is not the end of our relationship — it is the beginning. At The Lambert Agency, we perform regular policy reviews to ensure your IUL continues to perform as designed, and we are always available when your circumstances change or when you have questions.

11. Frequently Asked Questions About IUL Policies

The following questions are among the most commonly asked by clients across Austin and Central Texas when exploring Indexed Universal Life insurance. We answer each one with the directness and transparency that defines how we operate at The Lambert Agency.

How much does an IUL policy cost per month?

Premium costs for an IUL policy vary based on your age, health history, the death benefit amount, and how aggressively you fund the cash value. A healthy 35-year-old can typically fund a well-designed IUL for as little as $300 to $500 per month, while clients targeting maximum cash value accumulation may pay $2,000 to $5,000 per month or more. There is no universal answer — which is why we design each policy from scratch for every client.

Does an IUL policy have a savings account?

Yes — the cash value component functions similarly to a savings account in that it grows over time and can be accessed during your lifetime. However, unlike a savings account, the cash value grows tax-deferred and can be accessed via loans that are income-tax-free under current IRS law. It also earns interest linked to a market index rather than a fixed bank rate, giving it significantly higher long-term growth potential than traditional savings vehicles.

What happens to my IUL if I stop paying premiums?

IUL policies offer premium flexibility — one of their key advantages over whole life insurance. If you need to reduce or skip a premium payment, the policy can use accumulated cash value to cover the cost of insurance charges for a period of time. However, if the cash value is depleted and no premiums are paid, the policy will eventually lapse. Proper policy design accounts for this and builds in adequate cash value buffers. This is another reason why ongoing policy monitoring is essential.

Can I get an IUL policy if I have health issues?

Depending on the nature and severity of your health history, you may still qualify for an IUL policy — though possibly at higher premium rates. Some carriers specialize in higher-risk underwriting. We have helped clients across Austin with a range of health histories find coverage that genuinely serves their needs, and we are happy to explore all available options on your behalf.

Is an IUL policy right for someone who is close to retirement?

An IUL can still be a valuable tool for clients within 10 to 15 years of retirement, particularly for those with significant income and a desire to supplement their existing tax-deferred accounts with a tax-free income source. The accumulation timeline is shorter, which means premium levels will typically need to be higher to achieve meaningful cash value. A detailed illustration comparing your specific options is the only way to determine whether it makes sense for your particular situation.

How does an IUL policy affect my taxes when I pass it to my heirs?

The death benefit of an IUL policy passes to your named beneficiaries income-tax-free. For estates that may be subject to federal estate taxes — which in 2025 apply to estates above $13.61 million per individual — an irrevocable life insurance trust (ILIT) can be used to hold the IUL policy outside of your taxable estate. This is an advanced planning strategy that we coordinate in partnership with estate planning attorneys.

12. Is an IUL Policy Right for You?

After covering everything in this guide — from the mechanics of indexed crediting, to tax-free retirement income, to business owner applications, to living benefits, to the real risks you need to understand — the honest answer to “Is an IUL right for me?” is: it depends. And anyone who gives you a different answer without first taking the time to understand your complete financial picture is not doing their job.

An IUL policy is a powerful, flexible, and genuinely unique financial tool. For the right client, properly designed and consistently funded, it can be transformative — providing tax-free retirement income, protecting a family from catastrophic loss, growing business value, funding a child’s education, and leaving a meaningful legacy for the next generation, all within a single policy structure.

For other clients, a different product — or a combination of products — may serve their goals better. We will always tell you the truth about which path is right for you, even if that means recommending something other than what we have described in this article.

That is what it means to be an independent, client-focused agency. That is what it means to protect people, not just policies.

We are The Lambert Agency. We are based right here in Austin, Texas. And we would love to have a conversation with you.

TOP 5 QUESTIONS TO ASK A LIFE INSURANCE BROKER ABOUT IUL’S!

Question 1: “What is the cap rate, floor, and participation rate on this policy — and how have they changed historically?”

This separates honest brokers from salespeople. A broker who cannot clearly explain all three numbers, or who cannot show you how the carrier has managed those rates over time, is not someone you want designing your long-term financial strategy.

Question 2: “How is this policy designed — and are you maximizing cash value or death benefit?”

A poorly designed IUL prioritizes the death benefit, which increases internal costs and slows cash value growth. A properly designed IUL minimizes the death benefit within IRS guidelines to maximize cash value accumulation. If your broker cannot explain this distinction, that is a red flag.

Question 3: “What are the total internal fees and costs of insurance inside this policy?”

Every IUL has internal charges that come out of your premium before cash value is credited. A trustworthy broker will show you exactly what those fees are, how they change as you age, and what your net return looks like after all costs are factored in.

Question 4: “What happens to my policy if I miss a premium payment or need to reduce contributions?”

Life happens. A good broker will walk you through exactly how your policy handles premium flexibility, how long accumulated cash value can sustain the policy during a gap in payments, and what the worst-case scenario looks like if funding stops entirely.

Question 5: “Are you an independent broker, or are you captive to one carrier?”

This is perhaps the most important question of all. A captive agent can only offer products from one company. An independent broker like The Lambert Agency in Austin, Texas can compare IUL products across multiple top-rated carriers to find the policy that genuinely best fits your goals — not the one their employer tells them to sell.

The Lambert Agency

Austin, Texas | (512) 308-9319 | thelambertagency.com

Protecting People, Not Just Policies